Cover image via

Cover image via

Follow us on Instagram, TikTok, and WhatsApp for the latest stories and breaking news.

The recent closure of the Strait of Hormuz has sent shockwaves through the global energy market, creating a ripple effect that threatens the economies of vulnerable nations

When energy supplies are squeezed, low-income countries often bear the brunt.

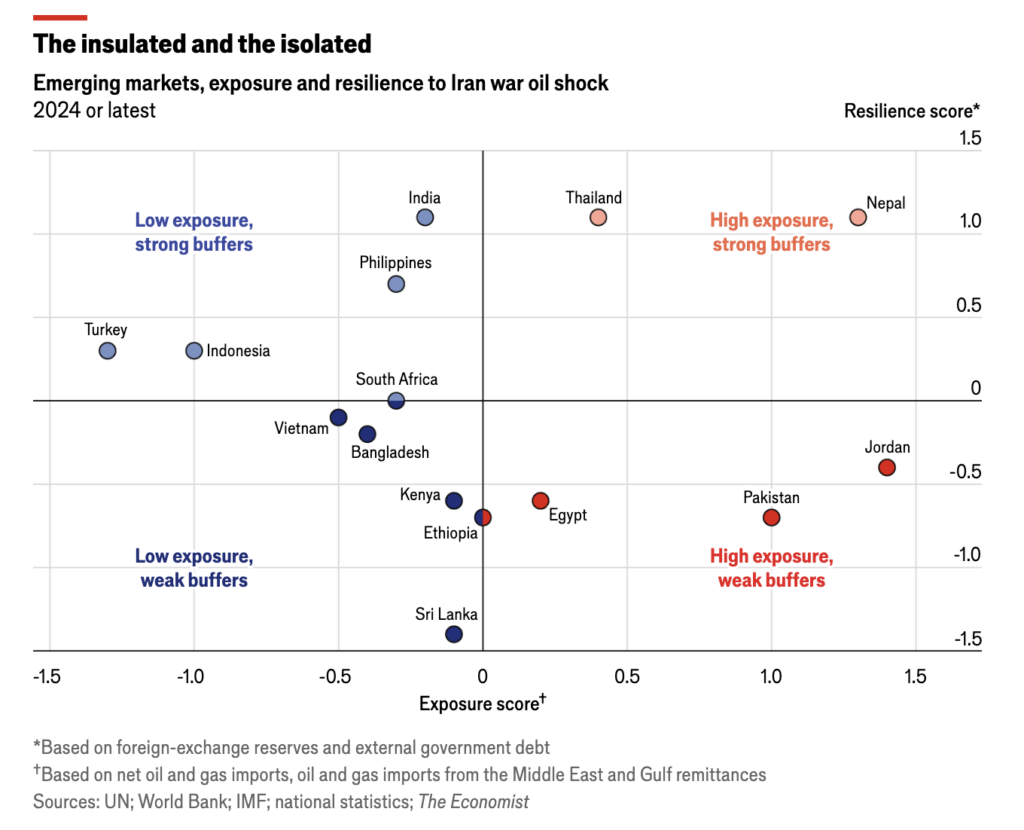

To gauge which countries are in the most precarious position, The Economist analyses data in two key factors: a country's exposure to the energy shock and its ability to absorb the financial blow.

• Exposure measures how heavily a nation relies on imported oil and gas, particularly from the Middle East, and its dependence on remittances — money sent home by citizens working in the Gulf.

• Capacity, or a country's financial "buffers", is determined by its foreign-exchange reserves and level of external debt.

A country with high exposure and low capacity is a prime candidate for a macroeconomic crisis, according to The Economist's analysis.

Here are the top 15 countries affected by the war in Iran:

1. Jordan

• Net oil and gas imports: 5.32% of GDP

• Oil and gas imports from Middle East: 90.6%

• Gulf remittances: 7.49% of GDP

• Foreign-exchange reserves: 7.8 months of imports

• External government debt: 42.11% of GDP

2. Pakistan

• Net oil and gas imports: 4.39% of GDP

• Oil and gas imports from Middle East: 88.8%

• Gulf remittances: 5.57% of GDP

• Foreign-exchange reserves: 2.8 months of imports

• External government debt: 25.07% of GDP

3. Sri Lanka

• Net oil and gas imports: 3.23% of GDP

• Oil and gas imports from Middle East: 43.5%

• Gulf remittances: 2.90% of GDP

• Foreign-exchange reserves: 2.9 months of imports

• External government debt: 41.81% of GDP

4/5 (tie). Egypt

• Net oil and gas imports: 2.86% of GDP

• Oil and gas imports from Middle East: 46.0%

• Gulf remittances: 5.48% of GDP

• Foreign-exchange reserves: 4.5 months of imports

• External government debt: 30.67% of GDP

4/5 (tie). Ethiopia

• Net oil and gas imports: 1.71% of GDP

• Oil and gas imports from Middle East: 97.0%

• Gulf remittances: 0.08% of GDP

• Foreign-exchange reserves: 1.8 months of imports

• External government debt: 22.46% of GDP

6. Kenya

• Net oil and gas imports: 2.83% of GDP

• Oil and gas imports from Middle East: 74.7%

• Gulf remittances: 0.31% of GDP

• Foreign-exchange reserves: 4.0 months of imports

• External government debt: 30.06% of GDP

7. Nepal

• Net oil and gas imports: 6.78% of GDP

• Oil and gas imports from Middle East: 51.4%

• Gulf remittances: 8.14% of GDP

• Foreign-exchange reserves: 10.4 months of imports

• External government debt: 20.93% of GDP

8. Bangladesh

• Net oil and gas imports: 2.23% of GDP

• Oil and gas imports from Middle East: 38.0%

• Gulf remittances: 2.78% of GDP

• Foreign-exchange reserves: 3.2 months of imports

• External government debt: 16.44% of GDP

9. South Africa

• Net oil and gas imports: 3.75% of GDP

• Oil and gas imports from Middle East: 48.6%

• Gulf remittances: 0% of GDP

• Foreign-exchange reserves: 5.7 months of imports

• External government debt: 22.32% of GDP

10. Vietnam

• Net oil and gas imports: 3.13% of GDP

• Oil and gas imports from Middle East: 37.5%

• Gulf remittances: 0% of GDP

• Foreign-exchange reserves: 2.4 months of imports

• External government debt: 9.55% of GDP

11. Thailand

• Net oil and gas imports: 7.25% of GDP

• Oil and gas imports from Middle East: 52.3%

• Gulf remittances: 0.03% of GDP

• Foreign-exchange reserves: 7.5 months of imports

• External government debt: 6.16% of GDP

12. Philippines

• Net oil and gas imports: 3.55% of GDP

• Oil and gas imports from Middle East: 25.6%

• Gulf remittances: 2.55% of GDP

• Foreign-exchange reserves: 7.3 months of imports

• External government debt: 15.80% of GDP

13. Indonesia

• Net oil and gas imports: 1.49% of GDP

• Oil and gas imports from Middle East: 15.9%

• Gulf remittances: 0.40% of GDP

• Foreign-exchange reserves: 5.7 months of imports

• External government debt: 16.84% of GDP

14. India

• Net oil and gas imports: 2.82% of GDP

• Oil and gas imports from Middle East: 51.4%

• Gulf remittances: 1.64% of GDP

• Foreign-exchange reserves: 7.5 months of imports

• External government debt: 5.50% of GDP

15. Turkey

• Net oil and gas imports: 0.64% of GDP

• Oil and gas imports from Middle East: 8.4%

• Gulf remittances: 0% of GDP

• Foreign-exchange reserves: 4.7 months of imports

• External government debt: 10.93% of GDP

Why are these countries vulnerable?

The ranking is not just about who imports the most oil. It's about the dangerous combination of high import bills and the lack of energy shock absorption preparedness.

Countries like Jordan, Pakistan, and Egypt top the vulnerability list because they are hit on both fronts. They are heavily dependent on Middle Eastern energy and also rely on billions of dollars in remittances from their citizens working in the Gulf.

As war disrupts the region, these remittance flows could shrink just as their energy import bills soar. This dual pressure strains their economy. With low foreign-exchange reserves (Pakistan's cover less than three months of imports) and massive debt payments (Egypt has a massive RM117 billion debt), both countries have very little room to absorb the shock.

Other nations like Bangladesh and Sri Lanka are also in a tight spot. Even with moderate exposure, their financial buffers are thin, noted The Economist. Similar to Pakistan, Bangladesh, which is currently on an International Monetary Fund (IMF) programme, only has reserves that barely cover three months of imports. Meanwhile, Sri Lanka only recently emerged from a 2022 default that was partially triggered by a previous energy crisis.

Conversely, some highly exposed countries are better prepared. Thailand spends a massive 7.25% of its GDP on energy imports, but it holds strong foreign reserves and a strategic oil reserve that can last for months. India is also expected to cope. While it gets over half its energy from the Middle East, it has strong reserves, can process different types of crude (including Russian oil), and relies more on domestic coal for electricity, shielding it from the worst of the price hikes.