Cover image via Chris Jung/NurPhoto/AFP & AFP

Cover image via Chris Jung/NurPhoto/AFP & AFPFollow us on Instagram, TikTok, and WhatsApp for the latest stories and breaking news.

Malaysia's medical insurance system is getting its biggest shakeup in years, and Bank Negara Malaysia has given the clearest picture yet of how it's going to work

In an interview with Berita Harian published today, 30 March, BNM Governor Datuk Seri Abdul Rasheed Ghaffour laid out the mechanics of the upcoming basic Medical and Health Insurance/Takaful (MHIT) plan.

He also spoke about a new protection that would stop insurers from arbitrarily rejecting your claims based on pre-existing conditions, and strict controls on how much they can charge.

Here's what you need to know.

BNM Governor Datuk Seri Abdul Rasheed Ghaffour.

Image via New Straits TimesWhy is this happening?

Only about 22% of Malaysians are currently insured, and 39% of total health spending in 2024 came from people paying out of pocket, cash from their own savings.

At the same time, the cost of private medical insurance has been rising sharply. Medical inflation is projected to hit 16% this year, up from an estimated 15% in 2025. For many Malaysians, especially older ones, premiums have become simply unaffordable.

There's also a trust problem.

Specialist doctors have raised serious concerns about insurers routinely using what some in the industry describe as "deny, delay, revoke" tactics, rejecting surgery, delaying emergencies, and revoking approvals even after care has been given.

Pre-existing conditions have been among the most commonly cited reasons for these refusals, even when the findings were incidental or unrelated to the illness being treated.

The new basic MHIT plan is BNM's attempt to fix all of this at once.

Bank Negara Malaysia, the country's central bank.

Image via AFPWhat is the basic MHIT plan?

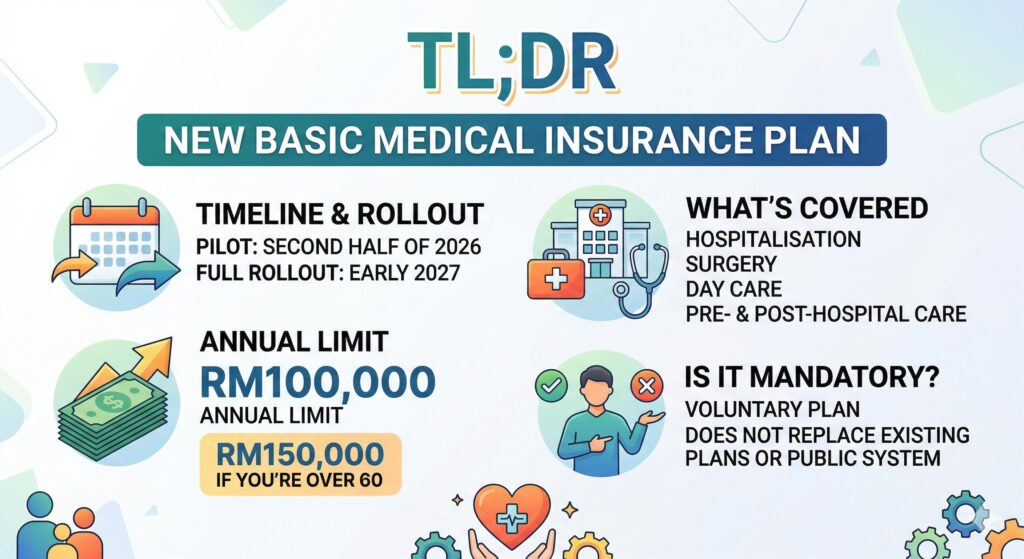

It's a standardised, government-designed medical insurance product that all participating insurers and takaful operators will be required to offer. Think of it as a baseline, a no-frills plan that's consistent, regulated, and designed to stay affordable long-term.

Key features include guaranteed renewal up to age 85 and gradual premium adjustments rather than sudden increases.

The plan sets an annual coverage limit of RM100,000, automatically increasing to RM150,000 for individuals above 60. According to BNM, in 2024, 99% of claims paid by insurers were RM55,225 or under, so for most people, that limit should be sufficient.

There are two tiers: a Standard Plan and a lower-cost Standard Plus Plan, which comes with higher deductibles.

The plan is voluntary, it doesn't replace your existing coverage, and it doesn't replace the public healthcare system. It fills a gap between public healthcare and high-end private coverage for those who want or need private hospital access.

The proposed "no look-back" clause: what it could mean and why it matters

This is one of the most significant measures BNM is studying for the new plan, but it's important to note that the details are still being worked out.

Under the current system, insurers can reject your claim based on pre-existing conditions, even ones you weren't aware of when you took out the policy. They can also deny claims on the grounds that you failed to disclose a medical condition, even if that condition is unrelated to what you're claiming for.

BNM is reviewing a "no look-back" clause that, if implemented, would mean insurers should no longer reject claims on the grounds of pre-existing conditions or previous nondisclosure — but only for conditions that are stable and well-managed. The clause is currently being studied together with industry experts before any finalisation.

At the same time, BNM is also reviewing a broader underwriting framework that would be more standardised, transparent, and fair across the industry.

The goal, as BNM has framed it, is to widen access for people with stable and controlled conditions, while keeping premiums affordable for everyone.

That balance is the core challenge.

Abdul Rasheed explained why insurers have historically restricted coverage for pre-existing conditions.

"ITOs usually exclude or limit pre-existing conditions to prevent people from obtaining coverage only after falling ill. Otherwise, it would increase claims and push premiums to unaffordable levels, which would also affect healthy customers," he said.

If the no look-back clause is implemented as proposed, Abdul Rasheed said it would provide meaningful assurance to policyholders.

"For policyholders, this provides long-term certainty and confidence that their coverage will be protected when they need it."

This matters a great deal in Malaysia, where chronic diseases are extremely common.

About one in six adults has diabetes, one in three has hypertension, and roughly a third have high cholesterol, and millions are unaware they have any of these conditions until they're tested. For those whose conditions are stable and controlled, this plan could be a genuine safety net.

One of the biggest anxieties around medical insurance in Malaysia is premium hikes: sudden, steep increases that force people, often older ones, to either pay up or drop their coverage entirely

Under the basic MHIT plan, premiums won't be set by insurers alone.

Abdul Rasheed said that product design, pricing structures, and coverage benefits will be standardised across the industry. Premium structures will be set by the regulator, taking into account actual claims experience and reasonable profit margins.

He was explicit that insurers are not permitted to impose additional charges or introduce features that could drive up the cost of these basic plans.

And if the system performs well, policyholders stand to benefit directly.

"Any improvements in claims experience over time will directly benefit policyholders through lower premium increase rates," he said.

For older Malaysians, the plan specifically aims to prevent being priced out of coverage. Premium adjustments due to medical inflation and ageing will be implemented gradually rather than in sudden spikes, and subject to periodic regulatory review.

Abdul Rasheed said the primary goal is "to ensure that the public can maintain coverage into their old age without facing sudden price hikes."

An employee talks on his mobile phone outside the lobby of Bank Negara.

Image via Tengku Bahar/AFPWhen is this happening?

The basic MHIT plan is scheduled for a pilot in the second half of 2026, with a full rollout targeted for early 2027, timed to coincide with the expiry of BNM's existing interim measures on medical insurance repricing.

Abdul Rasheed was clear about what the pilot is actually for.

"The focus during this phase will be on ecosystem readiness, including within the insurance and takaful sector and private hospitals. It will help identify technical issues, test operational readiness, and gather user feedback."

He added that any necessary adjustments to product structure, benefits, or the implementation timeline would be made before the full rollout.

Policyholders facing repricing will have the option to switch seamlessly to the basic plan with their current insurer, without new medical underwriting. EPF contributors will also have the option to use their Akaun Sejahtera savings to pay premiums, though this is entirely voluntary.

What this doesn't fix yet

The basic MHIT plan is a floor, not a ceiling. BNM has been clear that it's a starting point, simpler and more regulated than existing plans, but not a comprehensive solution to rising medical costs.

There are also open questions: the exact "no-look-back" waiting period hasn't been confirmed, final premiums won't be announced until closer to the 2027 launch, and the overall success of the plan depends heavily on how well private hospitals and insurers cooperate during the pilot.

The broader issue, that medical costs in Malaysia keep rising, isn't solved by a new insurance product alone. BNM has signalled this is part of a wider reform package, but those details are still being worked out.