Cover image via

Cover image via

Follow us on Instagram, TikTok, and WhatsApp for the latest stories and breaking news.

Buying a car in Malaysia is set to become much more transparent come 1 June

The amended Hire Purchase Act will officially come into force on 1 June 2026, marking the end of the "Rule of 78" and flat-interest rates.

This system has long been criticised for its lack of transparency and for penalising borrowers who sought to settle their loans early.

Domestic Trade and Cost of Living Minister Datuk Armizan Mohd Ali hailed these reforms as a cornerstone of the 2026 consumer movement agenda. But what does this actually mean for your wallet? And how do you calculate your car loan?

To illustrate the overhaul, let's look at a practical example: Sarah is planning to purchase a new vehicle priced at RM100,000

To keep things simple, let's assume the following figures:

- Vehicle Price: RM100,000

- Downpayment (10%): RM10,000

- Total Loan Amount (Principal): RM90,000

- Loan Tenure: Seven years (84 months)

- Effective Interest Rate (EIR): 4.5% p.a.

The EIR is the "all-in" price of your loan. While a flat rate might look cheaper on paper, the EIR is the more honest figure because it includes all fees and reflects the actual interest you pay as your debt decreases.

Under the amended law, banks are required to use the Reducing Balance Method.

Unlike the flat-rate system where interest was charged on the original RM90,000 loan amount for the entire seven years, interest is now calculated only on what you still owe.

Image for illustration purposes only.

Image via Polina Tankilevitch / PexelsStep 1: Calculating the monthly instalment

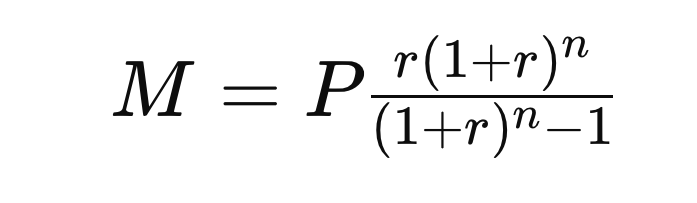

To find the monthly payment under the reducing balance method, the standard amortisation formula is used:

The standard amortisation formula.

Image via DLSD MortgageP = RM90,000 (Principal)

r = 0.00375 (Monthly interest: 4.5% ÷ 12)

n = 84 (Total months)

Sarah's monthly instalment: RM1,251.15

Step 2: Calculating the 'reducing balance'

The beauty of this law lies in how your monthly payment is split between interest and the principal. As your outstanding debt decreases, the interest charged also drops accordingly.

Month 1:

- Interest: RM90,000 × 0.00375 = RM337.50

- Principal Paid: RM1,251.15 – RM337.50 = RM913.65

- Remaining Balance: RM89,086.35

Month 2:

- Interest: RM89,086.35 × 0.00375 = RM334.07

- Principal Paid: RM1,251.15 – RM334.07 = RM917.08

- Remaining Balance: RM88,169.27

By the second month, Sarah is already paying less interest, allowing a larger portion of her installment to go towards her car's principal value.

The amended Hire Purchase Act is a win for consumers because it makes it a lot less painful to settle your loan early

The most significant pain point of the old "Rule of 78" was early settlement.

Under the old system, banks 'front-loaded' the interest, meaning your early payments went almost entirely towards interest rather than the car.

If you tried to sell your car after three years, you would often find the settlement figure shockingly close to the original loan amount.

With the 2026 Amendment, if Sarah decides to sell her car in Year 4, her settlement amount will be exactly what is reflected in her reducing balance statement.

There are no complicated rebate formulas that favour the bank.

Because she has been paying off the principal more aggressively from Day 1, her outstanding balance will be significantly lower than it would have been under the old law.