Cover image via

Cover image via

There's something oddly cruel about seeing your bank balance drop just days after payday

You thought you were being careful — but somehow, rent, Grab rides, bubble tea, and last weekend's brunch gang up on your wallet when you're not looking.

Most young Malaysians struggle with budgeting not because they're reckless, but because they're not aware of how to handle money properly. Between student loans, pressure to "enjoy life", and inflation creeping into every meal, it's no wonder our pay disappears so fast.

Image via designer491 (Canva Teams)

First things first, you can't fix your budget if you don't know where your money is going

Before you make any plans, you need to track your spending properly. It's not enough to guess. You'll be surprised how quickly little things like RM5 snacks or late-night online shopping start to drain your account.

Start by writing down every expense, no matter how small. Whether you prefer jotting it in a notebook, a spreadsheet, or an expense tracking app, the goal is the same — which is to get a clear picture of where your money is going.

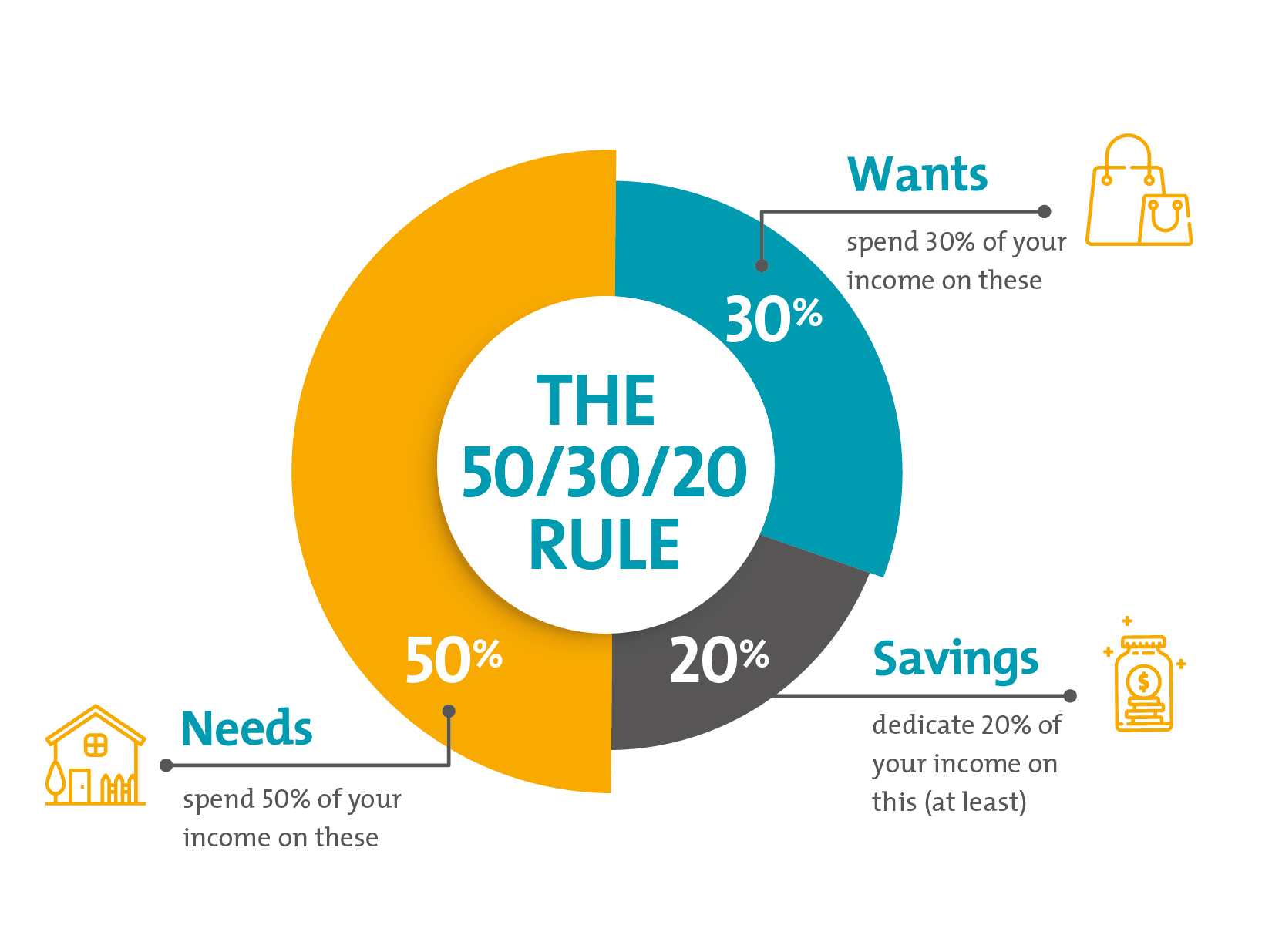

For those who haven't done any budgeting before, the 50/30/20 rule is a great place to start

Here's the basic formula:

- 50% of your income = needs (rent, bills, groceries)

- 30% of your income = wants (dining out, subscriptions, shopping)

- 20% of your income = savings and loan repayments

But this isn't a one-size-fits-all rule. If you're living in a city like KL or Penang, rent alone might take more than 50%. That's okay — you can always adjust the percentages to suit your situation, as long as you keep some room for savings.

Image via Infinity

Automate your savings so you don't have to rely on willpower

Pay yourself first. The moment your salary comes in, automate a transfer into your savings account. You can also split your account types — one for bills, one for savings, and one for spending. That way, you won't accidentally spend next month's rent on a new phone.

This also reduces decision fatigue. If you don't see the money, you won't be tempted to touch it.

Here's the thing no one really tells you — budgeting should include joy, or you'll hate every second of it

A good budget has room for enjoyment. If you try to restrict everything, you'll burn out or give up entirely. Instead, plan a small "fun fund" each month for guilt-free spending — whether it's a nice dinner, a short trip, or that movie you've been waiting for.

It's self-care, not irresponsibility.

Once you get the hang of budgeting, you should attempt to start an emergency fund

Whether it's a cracked laptop, car breakdown, or medical bill, you need a buffer. Experts suggest three to six months' worth of essential expenses, but if that sounds scary, start with RM500. Then, aim for RM1,000. You'll sleep better knowing it's there.

Image via Creativa Images/Canva Teams

You can still save money without cancelling your social life

Saving money doesn't mean isolating yourself or saying no to everything. Try switching to public transport a few days a week, cooking at home more often, or reviewing your unused subscriptions. It's about trimming the extras.

One thing you shouldn't do, however, is compare your finances to your friends. That is a one-way ticket to stress.

No one gets it right the first time, but the point is to start

The truth is, budgeting takes practice. You'll adjust the numbers every month, overspend occasionally, and question your life choices at 2am and that's normal.

What matters is that you're aware, proactive, and improving. Over time, you'll gain control not just over your money, but your life too.

Image via rattanakun (Canva Teams)